CNQ: Q1 Review and Political Headwinds

This company is a real beast. The stock has been under pressure for the last few years, but we see it heading (much) higher going forward.

Canadian Natural Resources (CNQ) continues to fire on all cylinders, cementing its position as the heavyweight champion of Canada’s energy sector. With 1.58 million barrels of oil equivalent per day produced in Q1 2025, $4.53B in adjusted funds flow, and $2.46B in net earnings, the company outpaces domestic peers in scale and profitability. But beyond earnings, CNQ's future hinges on access to international LNG markets. We investigate how Mark Carney will make or break this opportunity.

Here are the highlights of the last quarter:

1.58M boe/d production, up 19% YoY

Adjusted net earnings were C$2.436 billion, up from C$1.474 billion a year earlier

Higher sales volumes (+35%) and higher realized prices, with Q1 realized oil at ~$79.85/barrel and gas at C$3.13/Mcf

Realized synthetic crude oil operating cost was about C$21.88/bbl, which is $7–10/bbl below its peers

$1.8B returned via dividends (the 25th straight year of raises) and share repurchases

In short, cash flow and margins are at multi-year highs and the company is delivering strong shareholder returns despite a weaker price environment, as the breakeven WTI remains in the low–mid $40s/barrel.

Notably, a major concern is Canada’s dependence on U.S. markets. The U.S. has maintained a 10% tariff on Canadian oil and gas since March 2025. This raises costs for exporters. CNQ noted that widened oil differentials have already narrowed thanks to Trans Mountain, but any new U.S. trade barriers (or pipeline outages) could again disrupt flows. Management explicitly cited geopolitical trade uncertainty as a key issue in their outlook.

CNQ’s Positioning in the Energy Sector

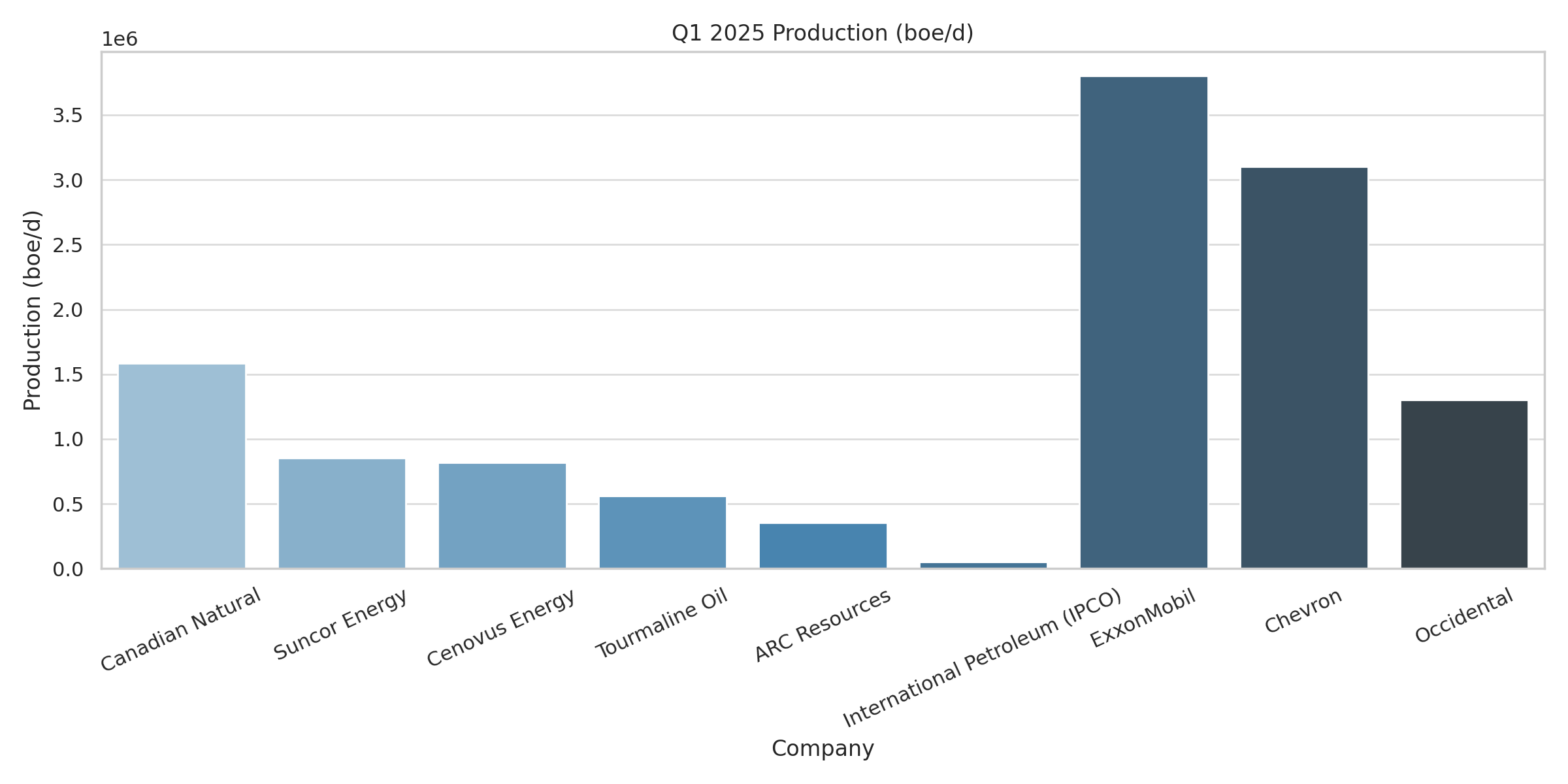

We compare CNQ with domestic and international peers in terms of output and profitability. We chose Suncor, Cenovus, and Tourmaline as comparable majors from Canada, and included the smaller ARC Resources and IPCO for illustrative purposes. Additionally, to compare the Canadian sector to its US peers, we added Exxon, Chevron, and Occidental to the comparison.

Canadian Natural is the largest oil and gas producer in Canada, and slightly bigger than Occidental. It gets dwarfed by the US giants Exxon and Chevron, however:

The chart looks pretty similar when comparing net earnings:

The most notable difference is that Exxon earned almost 5x as much as Canadian Natural (all numbers are in $CAD), despite only producing ~2.5x as many barrels. Similarly, Chevron earned four times more while producing twice as much oil. This is because US producers currently have stronger margins. Occidental Petroleum, which is Warren Buffett’s preferred oil stock, continues to look comparable to CNQ, with slightly weaker margins than its US peers.

In terms of domestic peers, Suncor’s Q1 results showed weaker refining margins, as its upstream cash flow was strong but R&M earnings fell on lower crack spreads. Cenovus saw refining gains but upstream realized lower oil prices, driving net income down. CNQ is more upstream-focused, which mitigates refining volatility but leaves it fully exposed to WTI and WCS price swings.

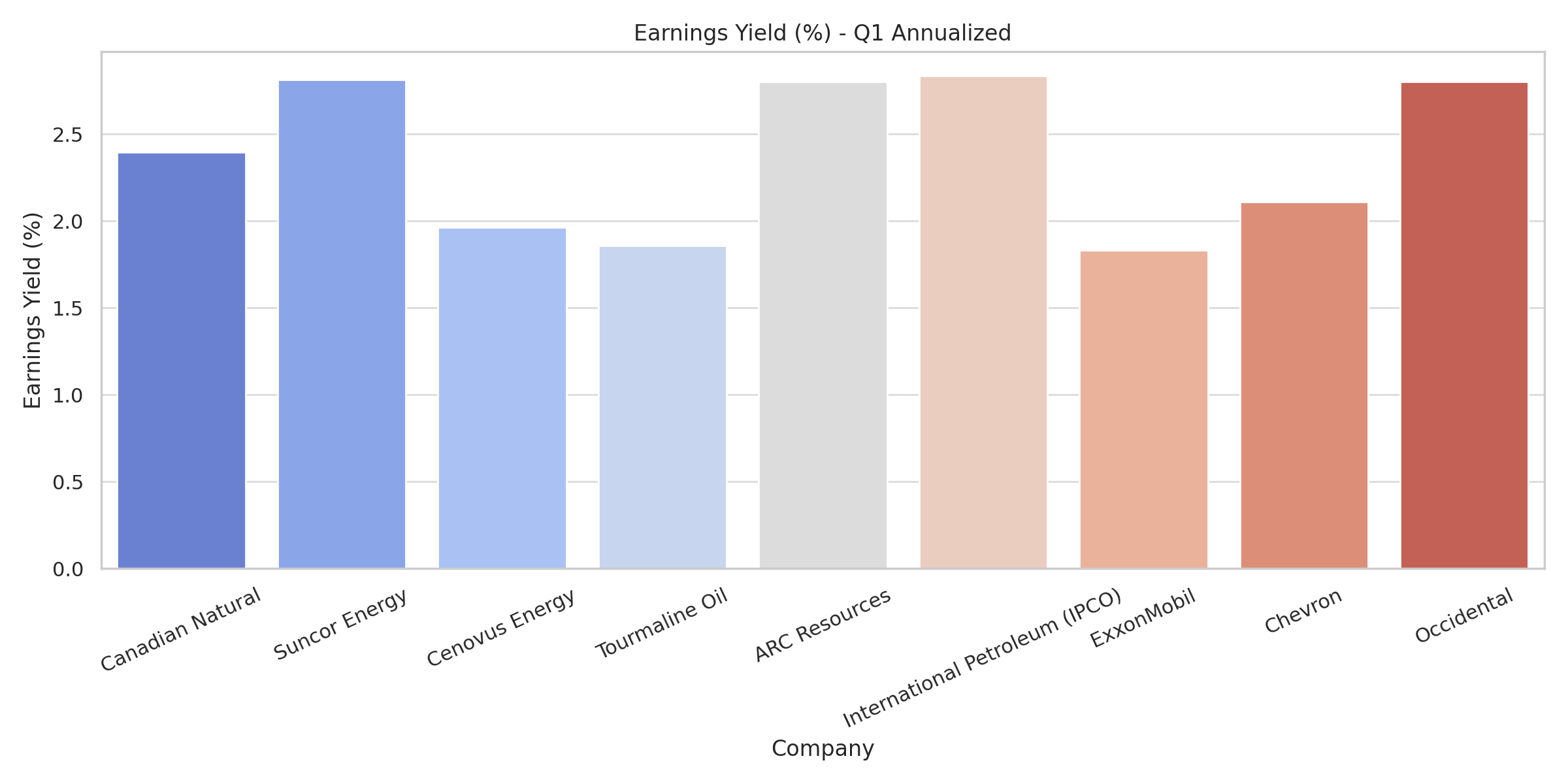

The Valuation Perspective

When stacked up against ExxonMobil, Chevron, and Occidental, CNQ looks modest in market cap but quite lean on valuation:

When annualizing Q1 earnings, CNQ shows a higher earnings yield than the two US giants and some domestic competitors. However, it falls short of Suncor, Cenovus, ARC, IPCO, and Occidental. This is probably why Buffett is in Occidental but not in Chevron or Exxon.

Taking into consideration that proven majors tend to trade at premiums compared to smaller competitors, this figure is quite surprising, and potentially an opportunity.

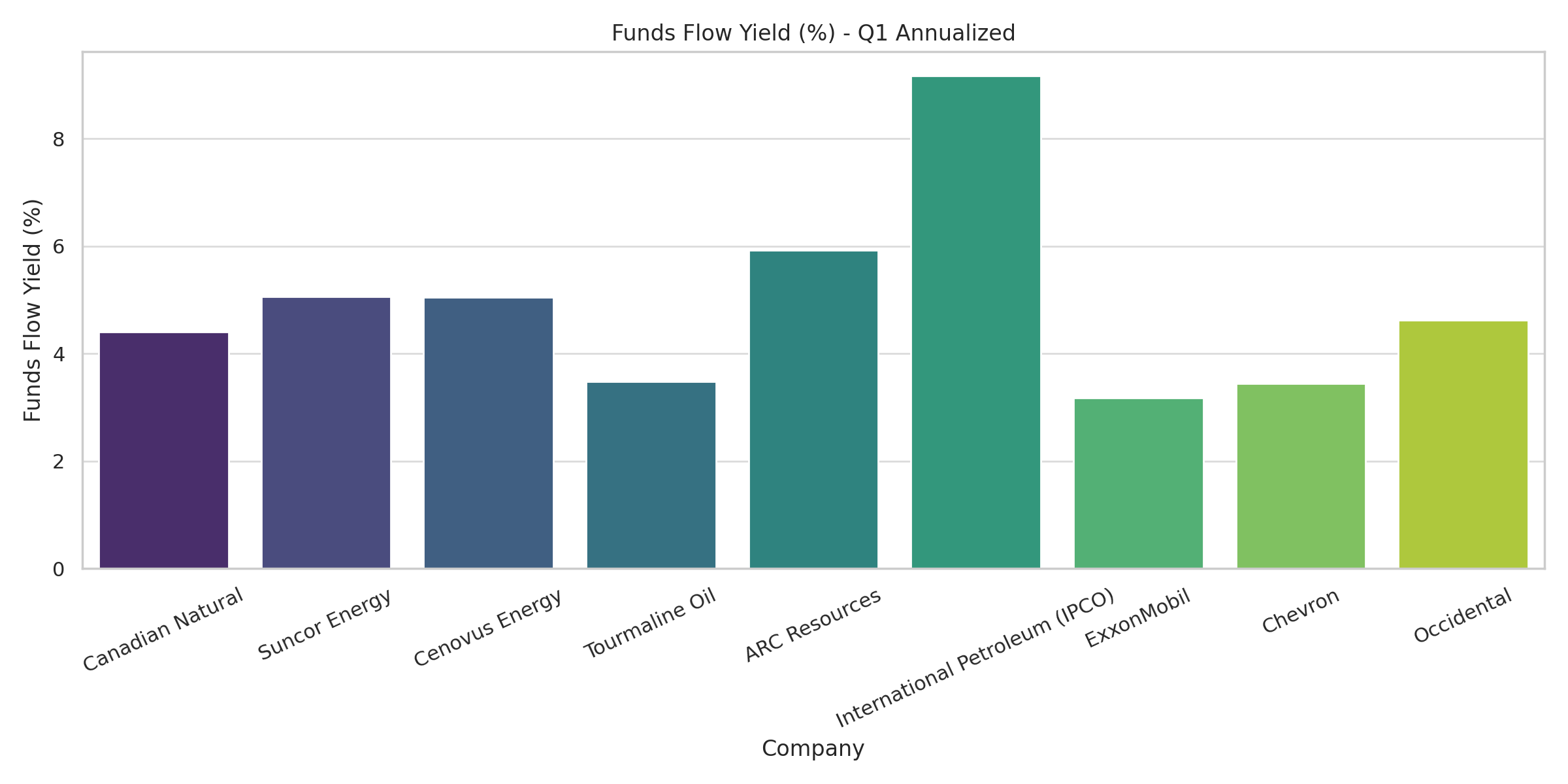

The annualized funds flow yields paint a similar picture, with the key difference being how much IPCO stands out in this comparison:

Is IPCO worth a second look, or is it cheap because it operates in high-risk jurisdictions like France?

Either way, Canadian Natural is, of course, not the cheapest stock in this list. Among its Canadian peers, it is pretty much in the middle on a valuation basis. However, it is trading somewhat cheaper than Exxon and Chevron, which it compares well to in terms of quality.

The Mark Carney equation

Mark Carney was probably not the favorite candidate of Canadian O&G equities during the April 30th election. And we can’t blame them — former Liberal PM Justin Trudeau made consistent efforts to undermine the Canadian oil and gas sector, to say the least.

Attempting to estimate the impact Carney will have on O&G is tricky. Pundits have portrayed him as a pragmatic man and a seasoned economist. His pedigree is indeed superior to that of his predecessor. However, in the fun game of politics, competence does not always rhyme with excellence.

Some of the statements made by the new man in power and his first actions can allow for an educated guess. Notably, one of his first actions was to scrap the consumer carbon tax, a levy implemented by his own party in 2019. Though the tax did not directly impact O&G equities, its removal is a positive signal for the sector and a relief for the broader Canadian economy.

During his campaign, Carney expressed a desire to make Canada more independent from the U.S. and to support the national oil and gas industry. In a speech in Calgary last April, he even vowed to make Canada “the world’s leading energy superpower.”1 But what kind of energy? From his campaign rhetoric, Carney appears more pragmatic than Trudeau, giving a prominent role to oil and gas in Canada’s short- and medium-term energy future.

That said, his words must be taken with a grain of salt. Carney was, after all, a politician on the campaign trail — trying to appeal to energy workers, conservatives, and his Liberal base all at once.

To better understand his position, we looked back at Carney’s earlier comments on the sector. In a 2023 interview, he stated: “The world is raising investments in clean energy, but oil and gas will still be necessary and will need investment to keep up with demand.” Yet, in other contexts, he’s made less O&G-friendly remarks. His convictions appear closely tied to the circumstances in which he operates, whether as head of impact investing at Brookfield or Special Envoy on Climate Action at the UN.

Only time will tell how the new PM will truly approach the sector. But while geopolitics certainly matters for O&G investors, we believe Canadian O&G equities will continue to thrive, even if Carney shows little support for conventional energy producers. The current strength of the sector is a testament to its resilience. Despite enduring strong headwinds during Trudeau’s decade-long mandate, these companies have managed to record solid earnings and reward shareholders. And we expect that to continue.

Conclusion

Canadian Natural had a strong quarter and is doing well even in the face of trade barriers. While the real headwind for the Canadian O&G sector has in recent years been its own government, as former PM Trudeau historically did not see a business case for it, we think that this situation could slightly improve under Carney. CNQ remains attractive in terms of profitability, scale, and valuation. It might be considered a “one size fits all” stock for investors looking to get exposure to Canadian oil and gas.

Thank you for reading. If you like our work, please like and subscribe. We aim to publish high-quality, timely updates on a variety of stocks in the natural resource space. And it’s free, which is a good price.

If you would like to support us financially, you are welcome to do so here:

https://oilprice.com/Energy/Energy-General/Carney-New-Oil-Gas-Investment-Is-Still-Needed-In-The-Energy-Transition.html