WHTW: June 16th - 22nd (War Special)

We monitored the situation extensively this week. Here is what happened.

Saturday night, Operation Midnight Hammer commenced. Seven US B-2 bombers flew for 18 hours to strike Iranian nuclear facilities at Fordow and Natanz, which means the US is now officially involved in this war. According to Chairman of the Joint Chiefs of Staff Dan Caine, the strikes inflicted “extremely severe damage and destruction.”

Some sources claim the sites had been evacuated in anticipation of the attack. Still, US Secretary of State Marco Rubio stated he doubted Iranian authorities managed to move nuclear material in time. He also emphasized that Washington was not planning any follow-up strikes. This aligns with JD Vance’s comments that the US is not at war with Iran, but rather “at war with Iran’s nuclear programme.” Trump, however, cited “Death to America” chants and said the US will take out more targets until Iran capitulates.

Meanwhile, Israel is not pausing. On Sunday afternoon, they launched new attacks on military targets in Bushehr. Predictably, Russia and China condemned the strikes.

In our view, Tuomas Malinen likely assessed the situation correctly in saying that “the desperate bombing of the Fordow and Natanz nuclear sites, which are so deep and so well fortified that no (conventional) bunker busters can reach them,” may have been conducted to buy time. “The Israelis may have threatened to nuke these sites,” he said on X. It is true that were Israel to deploy tactical nuclear weapons, this would likely cause a nuclear armageddon, as it would open the gates to new forms of attacks, with both sides having access to such weapons (through allies).

On the economic side, let’s revisit the Strait of Hormuz. In this week’s post on oil, we noted that the X rumours about it being closed were, to our knowledge, false. Those rumours have picked up again, with some accounts now claiming that a closure has been “approved by the parliament.”

We still believe that’s unlikely. Shutting the Strait would be economic suicide for Iran, and 75% of Asia’s oil passes through the Strait, so closing the Strait would essentially ensure that China (and Qatar) are not on their side either. And it's unclear whether parliament even has the legal power to enforce a closure. For now, traffic continues to move through the Strait.

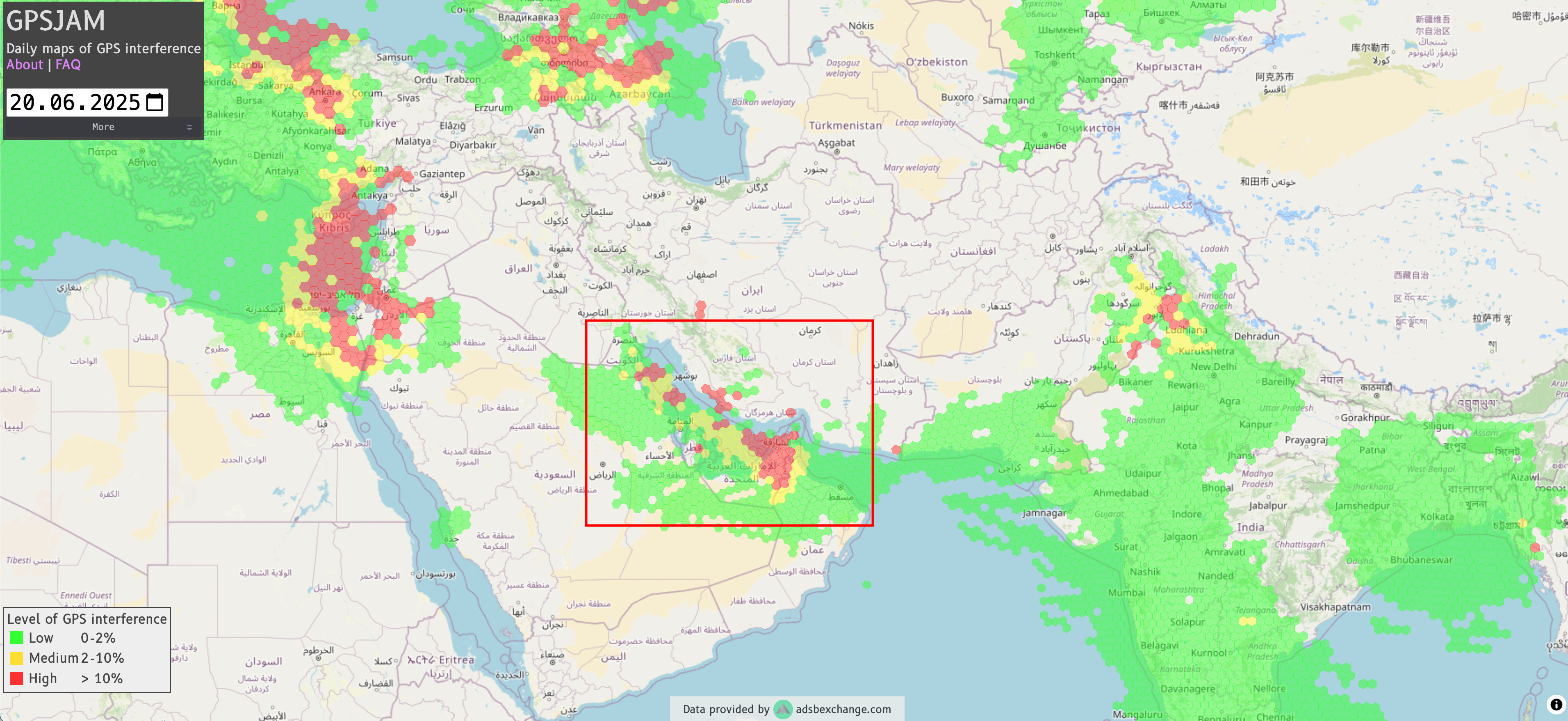

That said, we’re seeing elevated GPS jamming activity in the area; not a great sign.

Shipping companies may start to assess the risk differently. Some may pull out for now, unwilling to pay spiking insurance costs. For example, Greece’s shipping ministry has advised shipowners to “reassess passage” through the strait until the situation stabilises, but 175 Greek-owned vessels are currently still in the Gulf area. Others might simply gamble on the route staying open. As of now, it’s still operational.

Meanwhile, market reactions have been telling. PAX Gold ($PAXG), a cryptocurrency backed by gold that has previously served as a weekend proxy for gold’s moves in the following week, is up significantly, closing in on $3500, reinforcing gold once again as a safe haven.

Bitcoin, on the other hand, is acting like what it increasingly is: a high-beta, risk-on asset. It’s getting crushed on the news.

In other, more sector-specific news, the week wasn’t too exciting, but a few things happened:

Artemis Gold likely fired its CEO (or he may have resigned very abruptly), announcing that Mr. Dale Andres had been appointed Chief Executive Officer and Director of the Company, effective Monday. This development was rather unexpected considering Artemis’ stellar performance over the last few years. It has been a 4-bagger since the start of the bull run in February 2024.

Also, a few financings took place, including Cygnus Metals, Denarius Metals, Cassiar Gold, Solitario Resources, Golden Cross Resources, Cupani Metals, Trident Resources, and Goldstorm Metals. Talk about the sector being “underfinanced.”

Lavras Gold had a pretty good hit, intersecting 1.0 g/t Gold over 371 Metres at the Butiá Gold Deposit of their LDS Project in Southern Brazil

Global Atomic disappointed investors once again when they announced yet another C$30M private placement. They continue to reassure investors that DFC financing is “imminent,” and a JV is nearing final approval. Why might they need C$30M, then? Our stance on the company continues to be that it is a must-sell.

Also, Switzerland lowered its interest rates to 0%, following negative inflation in May. This, too, is bullish for gold and also makes the Swiss carry trade even more attractive.

Our view is however this war develops, the only two things we can be certain of are that it will cause volatility, and that gold (and possibly oil) will likely continue to do well. They might, however, encounter setbacks at any positive news inflow. We continue to stay almost fully invested and looking to add on dips. For now, most equities are near ATHs, so any cash we add to our brokerage accounts stays in 0-1 year treasuries or other kinds of short-term liquidity.

Thank you for reading. If this post was helpful to you, please consider liking and subscribing to our work. We aim to deliver timely, useful content for FREE.